Gamma Exposure (GEX): Why the Market Pins Some Days and Rips Others

Every move in SPX has two drivers. There's whoever's hitting buy and sell on the screen, and there's the dealer who sold them the option an hour ago and now has to hedge a position he never wanted. The second guy trades more size than the first, and here's the part most people miss: you can see exactly where he's about to get forced. That map is gamma exposure. Once you can read it, the random-looking chop in the middle of the day stops looking random.

Defining Gamma and Why It Matters

Gamma measures how fast an option's delta changes when the underlying moves. Delta is the first thing most traders learn: how much the option moves per dollar in the stock. Gamma is the next layer up. It tells you how fast that sensitivity itself is changing, which is really a measure of how badly a hedge has to be re-adjusted as price moves. An option with high gamma is one whose hedge won't sit still. A small move in the underlying flips it from barely sensitive to fully sensitive, and the dealer on the other side has to chase it.

is the option price, is spot. The thing to remember is the sign. If you own an option, you're long gamma. If you sold it, you're short gamma. Dealers are usually net short gamma to the crowd, which is the whole point: they're the ones forced to chase the hedge all day, not you.

Where Gamma Lives on the Chain

Gamma is biggest at the money and falls off fast in both directions.

At the money, gamma peaks. The option has no idea yet whether it's going to finish in the money or worthless, so its delta is jumpy and the dealer hedging is at its most aggressive. Far out of the money, gamma is basically dead. Delta is already near zero and barely moves. Deep in the money, same story for the opposite reason: delta is pinned near one and won't budge unless price makes a real move.

This is why a gamma wall is always one specific strike and not a zone. Gamma piles up exactly where the crowd is buying, and the crowd buys round numbers near the money.

Reading It as a Force

Think about what a dealer has to do to stay flat. When dealers are net long gamma at a strike, they sell into rallies and buy into dips to keep their book neutral. That flow leans against price and drags it back toward the strike. The strike turns into a magnet. When dealers are net short gamma, they do the opposite. They buy rallies and sell dips, which pours fuel on the move and shoves price away from the strike, usually in a hurry.

That's the whole engine behind “we pinned 5900 into the close” and “we knifed through 5850 the second it cracked.” Both are dealer hedging. One regime glues price in place, the other one lights it up.

Stable vs Wild

When dealers are net long gamma across the book, they're soaking up the crowd's directional flow. Ranges tighten, wicks get faded, realized vol prints under implied, and mean reversion works. When dealers are net short gamma, they're amplifying every push. Ranges blow out, fades get run over, realized comes in over implied, and trend is king.

Figuring out which of those two worlds you woke up in matters more than any setup you run inside it.

What Is Gamma Exposure (GEX)?

GEX takes that per-strike gamma, scales it into dollars, signs it by dealer positioning, and adds it all up. The standard formula per strike:

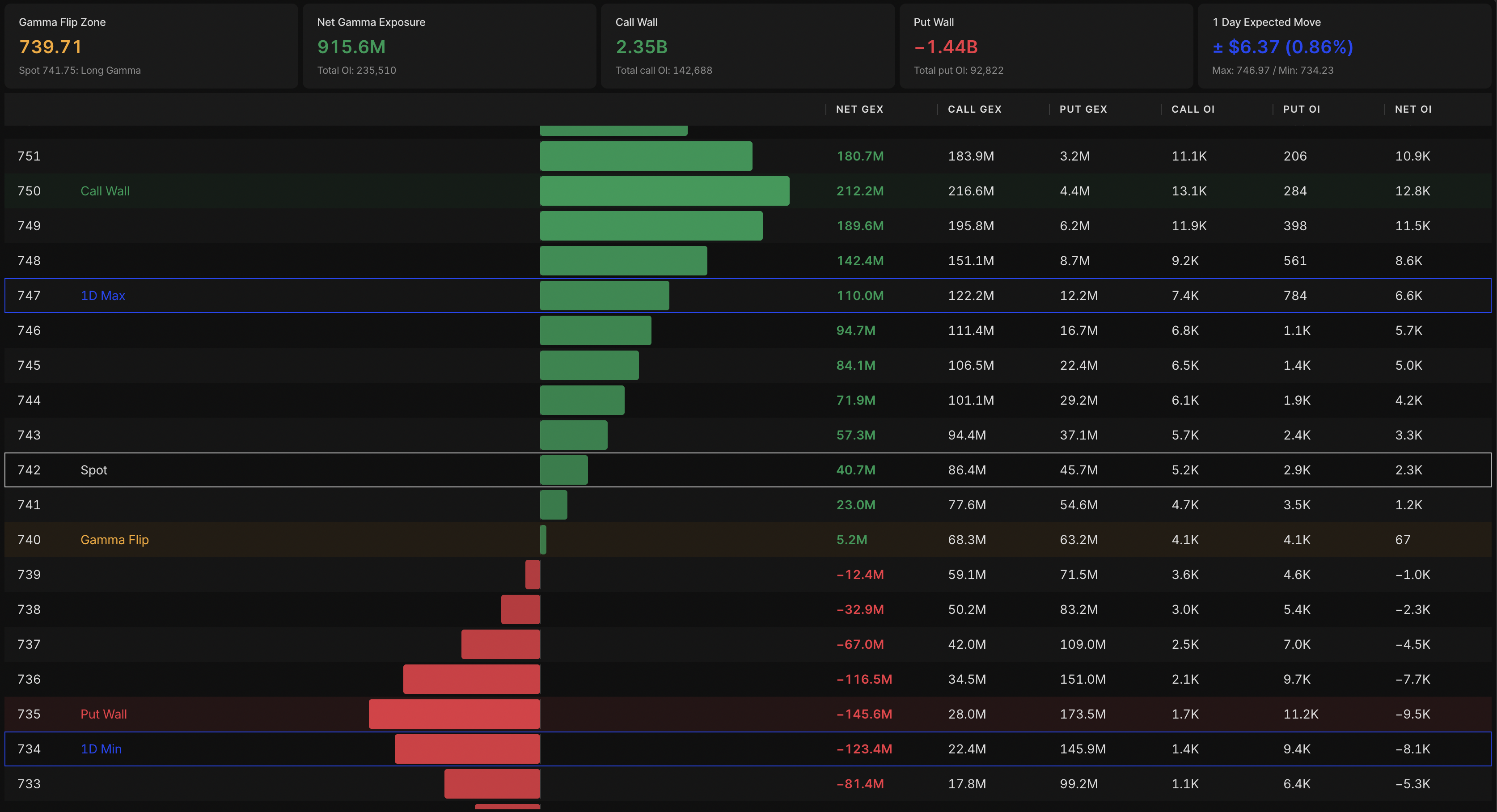

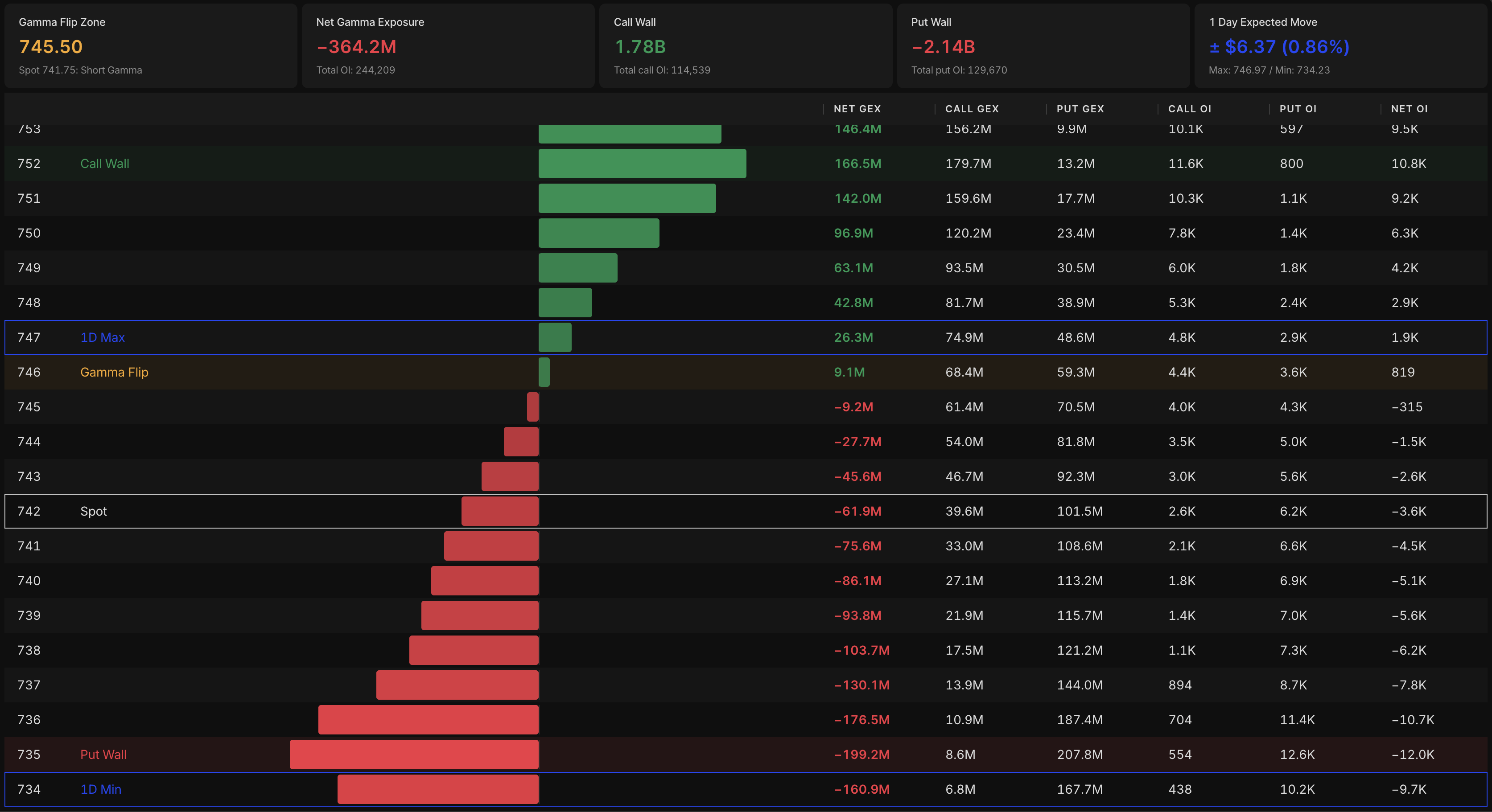

is the per-contract gamma at strike , is spot, is open interest there, is the multiplier, and is +1 for calls and −1 for puts. The sign convention comes from the usual assumption that dealers are short calls and long puts to the crowd. Add it up across every strike and you get a profile showing where dealer hedging is going to fire. Add it up across the whole chain and you get one number, the net market GEX, which is your regime switch.

Your Book vs the Market's Book

For one trader, gamma exposure is just the sum of your own positions' gammas. Long a Friday 600 call? You're long gamma, your delta climbs as price rises, and if you wanted to stay neutral you'd be selling stock against it. Most retail isn't running a neutral book, so personal GEX rarely comes up. It matters because it feeds the number that actually moves the tape: the market's.

Why the Whole Market Is the Edge

Market-wide GEX is the sum across every dealer's book at once, and this is where SPX and 0DTE traders make their money. There's something on the order of a trillion dollars of notional sitting in S&P dealer hedges at any given moment. When that aggregate is positive and stacked at strikes a couple percent from spot, the index trades like it's nailed down. Tight ranges, faded wicks, boring closes. When it flips negative, that same index trades like a small cap. Gap, run, gap, run. The macro didn't change. Dealer positioning did.

Generic options blogs talk about gamma one contract at a time. In SPX the entire game is reading it across the whole chain at once, which is exactly what Expo is built to show you.

The Punchline: GEX and Volatility

Positive GEX suppresses realized vol. Dealer hedging fights the crowd, implied bleeds out faster than people expect, and premium sellers eat. Negative GEX amplifies realized vol. Dealer hedging feeds the crowd, realized blows past implied, and the premium buyers and trend traders eat instead.

If you take one thing from this whole piece, take that. The sign of GEX is the switch for whether vol expands or dies. Everything else is detail.

Gamma Across the Strikes

At-the-money strikes carry the most gamma per contract, so heavy ATM open interest builds the strongest hedge force on the chain. Your Walls and your Flip usually sit right around there.

Far-OTM strikes carry almost nothing per contract, but size can override that. When retail call-bombs a name and stacks enormous OI on a 1%-OTM strike, the aggregate still bites. During those manias, watch cumulative OTM gamma, not just the per-contract number.

Deep-ITM strikes barely register. Delta is locked, gamma is gone, and nothing short of a real gap wakes them up.

Gamma and Time to Expiration

Long-dated options carry small gamma smeared across a wide band of strikes. Dealer hedging off them is slow and diffuse and rarely shows up as a clean intraday level.

Short-dated options are the opposite. Gamma gets concentrated and explosive. As expiry closes in, ATM gamma ramps hard, because there's less and less time for the question of in-or-out to resolve, so each dollar of spot matters more.

This is the entire reason 0DTE SPX behaves the way it does. A same-day option has gamma that dwarfs a monthly on a per-contract basis. Somebody buying 5,000 zero-dated calls at 5900 forces a hedge that, by the bell, can be the loudest flow of the whole session. If you trade daily SPX without a GEX read, you're staring at candles while everyone with an edge is trading the hedge underneath them.

Typical assumption: Dealers are short calls to the crowd, leaving them long gamma where call open interest is heaviest.

Effect: Hedging leans against the move. Rallies get sold, dips get bought, and spot gets dragged toward the high-gamma strike while the range squeezes shut.

Clustering: When call OI piles onto one nearby strike, the loop feeds itself. Price drifts in, the hedge accelerates the drift, and the move dies right at the level. That's your textbook OPEX pin.

Typical assumption: Dealers are long puts from the crowd, leaving them short gamma below spot.

Effect: Hedging feeds the move. Down forces more selling, up forces more buying, and realized vol expands.

Clustering: When put OI stacks below spot and price breaks through, it cascades. Dealers selling into a falling tape look exactly like forced liquidation, because mechanically that's what it is. The February spikes, the August unwinds, most of the “out of nowhere” SPX flushes all look the same in the GEX profile the morning they happen.

How Dealers Get Trapped Into Moving the Market

They take the other side. Every option the crowd trades needs a counterparty, and the dealer is it. He inherits the crowd's exposure flipped: long puts when they buy puts, short calls when they buy calls.

They have to stay neutral. Dealers aren't betting direction. They're skimming the spread thousands of times a day and staying flat by hedging the inherited delta in the underlying. That hedge is not optional. Real risk limits force it every single time.

They become the gravity. Because the hedge is constant and the size is enormous, the hedging itself turns into a price force. Heavy-gamma strikes pull (positive regime) or push (negative regime). This isn't a theory you have to believe. It's just what the math does when you run that much size through it.

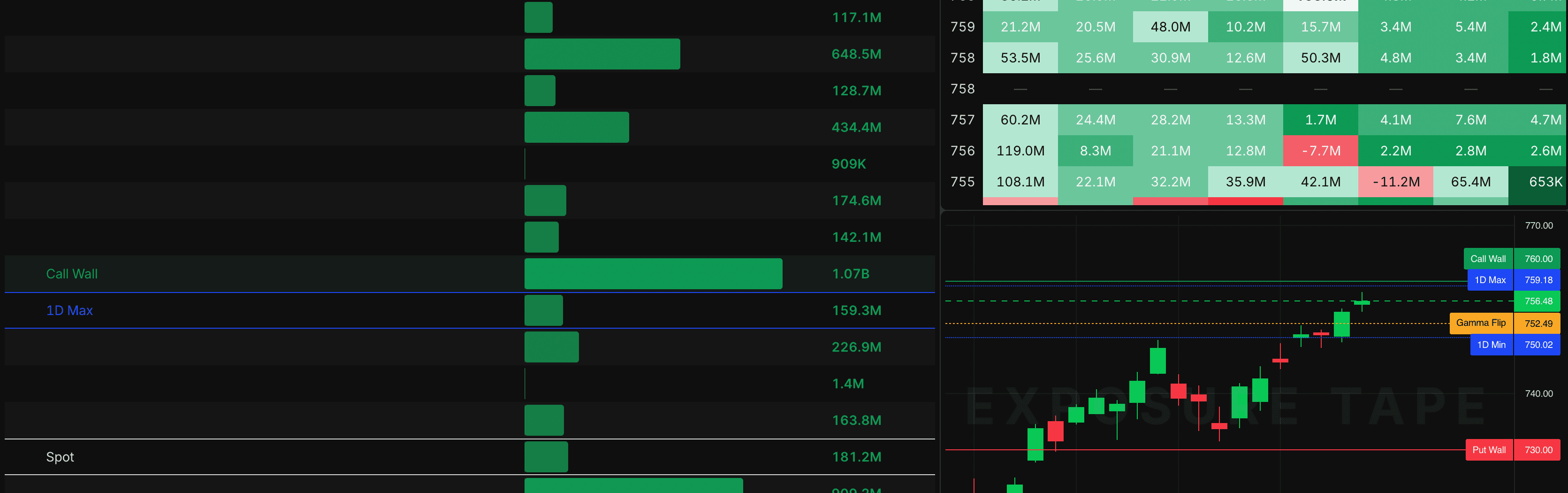

Gamma was stacking up at 5950 through the first hour. By 11:00 ET the Expo profile had net gamma at that strike bigger than anything else within a percent of spot. Price ground from 5942 up to 5949 by 12:30, tagged the level, and stalled.

For the next two and a half hours every poke at 5950 got sold and every dip back to 5945 got bought. Three-point range, way too tight for an SPX session at that VIX. Into the close, price pinned at 5949.50. The 5950 strike held all afternoon as support on the dips and resistance on the rips. That wasn't some line a chartist drew. It was the strike where the dealer book was forced to fade everything in both directions, and the tape did exactly what the hedge math said it would.

Why This Matters

These aren't random intraday wiggles. They're structural flows. A candle-only trader sees a tight-range day, shrugs, and moves on. A GEX trader saw the strike that was going to run the day before the day even opened. He sizes for it, sells premium against the level if the regime is positive, fades the wicks instead of chasing them, and gets out before the regime can roll over into the afternoon. The candle is the result. The flow is the cause. GEX is the only read on the cause that retail can actually get.

How This Shows Up in the Wild

Gamma Squeezes in Single Names

The original GME and AMC runs were gamma feedback loops in a negative-gamma world. The crowd bought far-OTM calls in size. Dealers, short those calls, had to buy stock to hedge. The buying pushed price toward the strikes, which raised the calls' gamma, which forced dealers to buy even more. Round and round until the calls expired or got unwound. Every single-name squeeze rhymes: a pile of OTM call OI, dealers short gamma, a catalyst that cracks the dam, then a near-vertical rip as the hedge loop compounds on itself.

Daily SPX and Intraday Vol

0DTE SPX is the most gamma-sensitive thing trading anywhere. A one-day ATM option has gamma orders of magnitude bigger than that same strike at 30 days out. So when the 0DTE chain loads up one-sided, say a Tuesday where retail floods the 5950 calls, the afternoon hedge does one of three things: a slow grind into the strike and a pin (positive regime), a hard reject when price can't get there and the premium bleeds out, or a clean break through followed by a spike as the regime flips from positive to negative the moment spot clears the biggest-OI strike. Reading 0DTE GEX at 9:31 tells you which one to expect. The candle tells you which one happened, three hours too late to do anything about it.

Around Monthly OPEX

Monthly expiration wipes the gamma book in a single session, so a regime that held for two weeks can flip Monday morning when the new front-month chain takes over. Always re-read GEX the day after OPEX. And expect pinning into the close on the big day. The fattest open-interest strikes turn into magnets, and the cash often settles within pennies of the dominant ATM strike. The third Friday is not a normal trading day, so plan for it.

Walls, Ladders, and Where Price Gets Stuck

Call Ladders

A call ladder is a stack of big positive-gamma strikes sitting above spot, each one acting like a ceiling. Price rises, hits the first, stalls. Punch through and the next one up is the next ceiling, same mechanic a little higher. That's where the stair-step rallies in SPX come from. They aren't chart patterns. They're dealer hedge levels you could see in the GEX profile before a single one of those candles printed.

Call Resistance and Put Support

The biggest positive-gamma strike above spot is the Call Wall, where dealers' short-call hedging caps rallies. Drift into it slowly and you get sold. Hit it on a momentum sweep and you can blow through, and once you do the wall often flips into a floor on the way back, because the same hedging that capped the rally now buys the dip back to the level.

The biggest negative-gamma strike below spot is the Put Wall. Put OI there is so heavy that any flush into it gets bought. Dealers long puts are short gamma at that strike, so a move down toward the wall trips their buy-side hedge and holds the level. Walls aren't technicals. They're the strikes where the hedge math is concentrated, and they move every session as open interest shifts under them.

Trading It on Zero-DTE

Gamma is enormous and still climbing. A 0DTE ATM option can see its gamma double in the last half hour, which makes the closing hedge the most violent flow of the day. Even small price moves trigger oversized stock-side adjustments. Size for that.

Stops are brutal. A 0DTE position can swing 30% in three minutes around a flip. A stop set against a 1% spot move can get vaporized by a 0.1% move on the right strike. Either trade defined-risk structures like verticals and condors (the Strategies product is built for exactly this) or accept your stops run wider than your usual daily tolerance.

The asymmetry is the whole thing. A 0DTE trade lined up with the GEX regime and on the right side of the Wall can double in twenty minutes. The same trade fighting both is a slow, controlled donation. The gap between regime-aligned and regime-fighting on zero-dated is bigger than any setup edge you'll find anywhere else, so respect it.

Where GEX Gets It Wrong

GEX leans on one assumption: dealers are net short calls and net long puts from crowd flow. That holds up for SPX, SPY, QQQ, and the big Mag 7 names in a normal tape, where flow is dominated by call-buying and put-buying and dealers fill both sides. It breaks when flow does something structurally weird. A Friday where retail call-bombs one name can overwhelm the usual dealer-short-call assumption, and the GEX sign at that strike can be flat wrong. Watch for it in squeeze setups and obvious retail manias. For the index, the assumption is sturdy enough that the regime read holds up across nearly every session.

Thin Names and Stale OI

On thin names there are two more failure modes. Low-priced stocks with dollar-wide strike spacing throw GEX profiles dominated by a couple of high-OI strikes that may not reflect the real dealer book, so treat sub-$20 names with suspicion. And stale OI, especially in the roll period right after expiry before old strikes get cleaned out, can show up as gamma nobody is actually hedging. Expo filters those by requiring a live bid/ask before it counts a strike. Rougher tools don't, which is where the ghost levels come from.

Key Takeaways for Traders

| Step | Action | Why it matters |

|---|---|---|

| Identify | Open Expo at the start of the session. Mark the Call Wall, Put Wall, and Gamma Flip. | These are the strikes where hedging fires, and they tell you the regime you're trading inside. |

| Watch behavior | See how price acts at each level. Does it fade into the Walls or punch through? Does the Flip hold? | Confirms or kills the regime read live. How price behaves at the levels is the tell. |

| Align the trade | Trade with the regime. Sell premium into Walls when positive, take directional when negative, skip mean-reversion on a Flip break. | Structural flow beats setups. A regime-aligned trade is hedged by the dealer book itself. |

| Manage risk | Size for gamma. Cut 0DTE size more than feels necessary. Use defined-risk structures around the Walls. | Gamma compounds both your wins and your losses. The shorter the DTE, the tighter the discipline. |

| Journal it | Log the GEX setup at the open. Regime, Walls, Flip. Compare to how the session actually played out. | Pattern recognition is the only edge that lasts. Two months of journaled setups recalibrates everything else you do. |

A few honest caveats

- GEX is structure, not timing. It tells you which strikes matter and what regime you're in. It will not tell you the minute the move starts. Pair it with a flow read like Heat or a clean price trigger.

- Don't trade it alone. The best setups stack: regime-aligned GEX, confirming Heat flow, and a price trigger at the Wall. Any one by itself is a coin flip. All three together is the trade.

- It can flip fast near OPEX. Monthly expiration clears the book, and the regime that held all week might be gone Monday. Always re-read the profile the session after a big expiration cycle.