Delta Exposure (DEX): Which Way the Tape Leans

Gamma tells you where price gets stuck. Delta tells you which way it wants to drift between those points. Every option a dealer holds carries a directional weight, and to stay flat he has to trade the underlying against it all day long. Add that hedging up across the whole chain and you get the market's lean: the path of least resistance for spot before a single candle prints. That number is delta exposure.

Defining Delta and Why It Matters

Delta measures how much an option's price moves for a $1 move in the underlying. It is the first derivative of the option price with respect to spot, and the most useful way to read it is as a hedge ratio: the number of shares a dealer must hold per contract to stay directionally flat. A 0.40-delta call behaves like 40 shares of stock. Sell that call and you are short 40 shares of exposure you did not want, so you buy 40 shares to neutralize it.

is the option price, is spot. Calls carry positive delta (0 to +1), puts carry negative delta (0 to −1). The thing to hold onto: delta is not static. It moves as spot moves, as time passes, and as vol shifts, which means the dealer's hedge is never done. That constant re-hedging is the flow this whole post is about.

Where Delta Lives on the Chain

Delta is a smooth curve from 0 to ±1, and where an option sits on it depends on moneyness.

At the money, delta is about ±0.50: the option is a coin flip, and it behaves like roughly half a share. Deep in the money, delta approaches ±1: the option moves nearly dollar-for-dollar with the stock, so the dealer hedge is close to a full share and barely changes. Far out of the money, delta approaches 0: almost no directional weight, almost nothing to hedge.

The strikes that move the dealer book are the ones where delta is meaningful and open interest is heavy, which clusters around and just out from spot. That is where DEX is built.

Reading It as Direction

Gamma is about magnitude: how hard price gets pinned or released. Delta is about direction: which side the dealer book is leaning and which way its hedging pushes. When a dealer is short calls to a call-buying crowd, he is short delta, so he buys stock to hedge. That buying is a bid under the tape. When he is short puts to a put-buying crowd, he is long delta, so he sells stock to hedge. That selling is an offer over the tape.

So the net delta the dealer book carries is not a passive number. It is a standing instruction to buy dips or sell rips, and that instruction is the lean.

A Bid Under, or an Offer Over

When dealer hedging is net a bid, dips get absorbed and the path of least resistance tilts up. When it is net an offer, rallies get sold and the tilt is down. Knowing which one you woke up to is the difference between buying the dip and catching the knife.

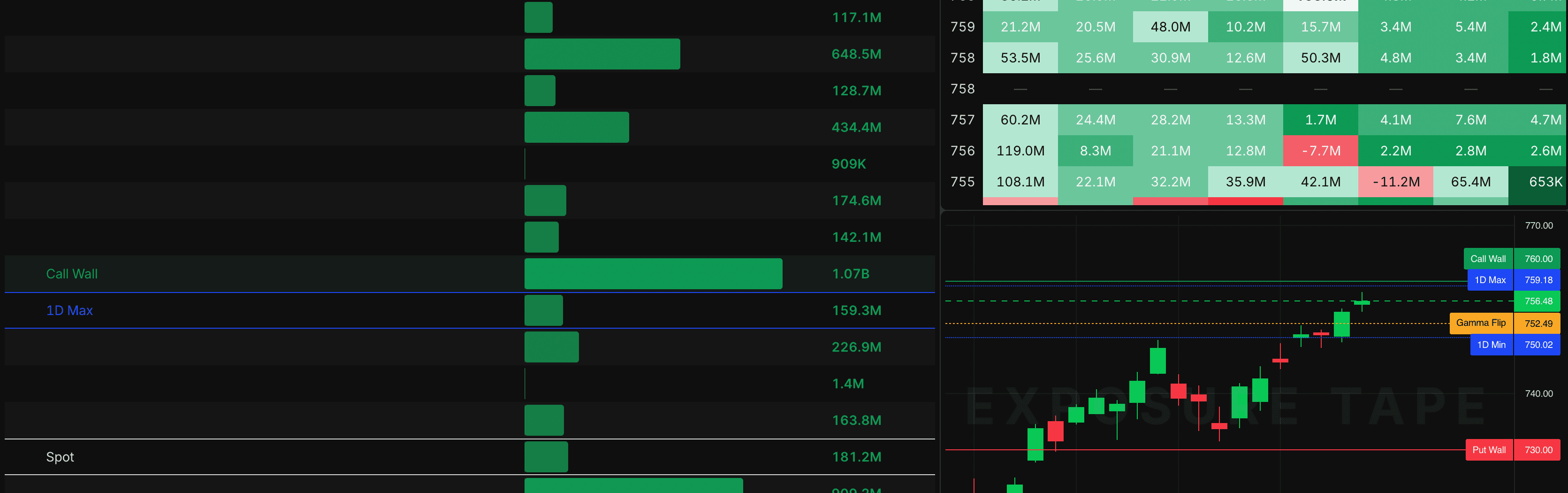

What Is Delta Exposure (DEX)?

DEX takes every contract's delta, weights it by open interest, converts it to dollars, signs it by dealer positioning, and sums the chain:

is the per-contract delta at strike , is open interest there, is the multiplier, and is spot. The sign convention flips customer exposure to the dealer side: dealers are the inverse of the crowd, so when customers are net long delta, dealers are net short it. Sum to one number and the sign is your read. Positive DEX means the dealer book is a net bid; negative DEX means it is a net offer.

Your Book vs the Market's Book

For one trader, delta exposure is just the summed delta of your positions, the number your broker shows as net delta. Useful for sizing, but it is not what moves the index. The number that moves the index is the aggregate across every dealer hedging at once.

Why the Whole Market Is the Edge

Market-wide DEX is the net delta the entire dealer complex carries from customer flow. In SPX that is an enormous, slow- moving bid or offer that sits under the tape all session. When it is firmly positive, dips into the book get bought and the index grinds; when it flips negative, the bid disappears and air pockets open below. The macro headline did not change. The lean did. Reading it across the whole chain, which is exactly what Expo is built for, is the edge generic one-contract delta talk never gives you.

The Punchline: DEX Is the Lean

Positive DEX: dealer hedging is a standing bid, dips get bought, path of least resistance up. Negative DEX: dealer hedging is a standing offer, rallies get sold, path of least resistance down.

That is the whole point. GEX tells you the levels; DEX tells you which direction price drifts between them.

Delta Across the Strikes

ATM strikes sit near ±0.50 delta. With heavy open interest, these carry real directional weight and they are the most reactive, because their delta swings fastest as spot moves through them.

Far-OTM strikes carry almost no delta, so individually they barely register. But when the crowd stacks enormous OI on a near-OTM strike, the aggregate delta there can still tilt the book.

Deep-ITM strikes carry near ±1 delta but rarely trade in size, and their delta is stable, so they anchor the book without moving it. The action is always around spot.

Delta and Time to Expiration

Long-dated deltas are stable. An option months out shifts its delta slowly as spot moves, so the hedge is calm and DEX built from it drifts rather than jumps.

Short-dated deltas are violent. Because gamma is huge near expiry, a small spot move flips a near-ATM option from 0.30 to 0.70 delta in minutes, and the dealer has to chase the hedge to match. That is why 0DTE DEX can swing from a firm bid to a firm offer inside a single hour. If you trade daily SPX, the delta lean you read at 9:31 is not the lean at noon. Re-read it.

Typical assumption: Customers are net long delta (call-heavy), so dealers are net short delta and have to buy stock to hedge.

Effect: That hedge buying is a persistent bid. Dips get absorbed and the path of least resistance tilts up.

Clustering: When call OI concentrates just above spot, the bid stacks there. Price grinds up into it on low volatility, the classic slow-melt-up tape.

Typical assumption: Customers are net long puts, so dealers are short puts, long delta, and have to sell stock to hedge.

Effect: That hedge selling is a persistent offer. Rallies get faded and the path of least resistance tilts down.

Clustering: When put OI concentrates below spot and the bid vanishes, a break lower finds no support and the dealer selling compounds the move. That is the air-pocket flush.

How Dealers Get Trapped Into Moving the Market

They take the other side. Every option the crowd trades needs a counterparty, and the dealer fills it, inheriting the crowd's directional exposure flipped.

They have to stay neutral. Dealers are not betting direction. They earn the spread and hedge the inherited delta in the underlying. That hedge is forced by risk limits, not a choice.

Their hedge becomes the lean. Because the net delta is huge and the hedging is continuous, the aggregate buying or selling is itself a standing directional force in the tape. DEX is the retail-visible read on which way that force points.

On June 5, SPY opened with net dealer delta firmly positive on the Expo profile, the heaviest call OI stacked at 600 just above a 598 spot. The read was simple: a bid under the tape, drift up. For the first two hours every pullback to 597.50 got bought within minutes, the range was tight, and spot ground to 599.80 by noon without a single real flush.

The grind was not momentum and it was not news. It was the dealer bid doing exactly what positive DEX said it would: absorbing supply on every dip until price reached the strike where the call OI sat. A trader reading the candle saw a boring up day. A trader reading DEX knew the dip was buyable before the open.

Why This Matters

These are not random drifts. They are structural flows. A candle-only trader sees a slow up day or a sudden flush and reaches for a story afterward. A DEX trader saw the lean before the open, bought the dip when the book was a bid, and stood aside when it flipped to an offer. The candle is the result. The dealer delta is the cause. DEX is the only read on that cause retail can actually get.

How This Shows Up in the Wild

Delta Squeezes in Single Names

When a single stock gets call-bombed, dealers go heavily short delta and have to buy stock to hedge. That buying lifts price, which lifts the calls' delta, which forces more buying. The same feedback that drives a gamma squeeze shows up first as a one-sided, runaway dealer bid in the delta read, the directional fuel under the squeeze.

Daily SPX and Intraday Lean

0DTE flow rewrites the SPX delta book hour by hour. A morning that opens call-heavy (positive DEX, dealer bid) can flip to put-heavy by the afternoon as the crowd hedges a fade, and the bid that held all morning simply turns off. The flushes that look like they came from nowhere usually came from the delta book flipping negative in plain sight. Read DEX at the open to set your bias, and re-read it whenever the tape changes character.

Options Expiration (OpEx) Effects

Monthly expiration clears a huge slug of delta out of the book in one session, so the lean that held for two weeks can vanish Monday morning when the new front-month flow takes over. Always re-read DEX the session after OPEX before you trust yesterday's bias.

Direction Plus Levels: DEX With GEX

DEX on its own tells you the lean, not where it stops. That is what gamma is for. The strongest reads pair the two: DEX gives you the direction of least resistance, and the Call Wall and Put Wall from gamma exposure give you the levels the drift is heading toward and where it is likely to stall.

Positive DEX into a Call Wall above is a grind that fades as it nears the wall. Negative DEX with a thin Put Wall below is a flush with nothing to catch it. Direction times levels is the trade; either one alone is half the picture.

Trading It on Zero-DTE

The lean is real but it is fast. 0DTE delta swings hard because gamma is enormous near expiry, so the dealer bid that supported the first hour can become an offer by the second. Treat the DEX read as a short-shelf-life bias, not a set-and-forget direction.

Size for the flip. A position leaning with positive DEX can get run over the moment the book goes negative, and on zero-dated that happens in minutes. Use defined-risk structures like verticals (the Strategies product is built for it) or keep stops honest and tight to the read that put you in.

Pair it with the real-time flow. DEX is the positioning snapshot; the minute-by-minute version of the dealer delta hedge is what Heat plots live. Snapshot for the bias, flow for the trigger.

Where DEX Gets It Wrong

DEX rests on the same flow assumption as the rest of the dealer- positioning toolkit: that customers are net buyers of calls and puts and dealers take the other side. That holds for SPX, SPY, QQQ, and the big Mag 7 names in a normal tape. It breaks when flow is structurally one-sided, like a name being call-bombed by retail or an institution selling covered calls in size against stock, where the dealer-inverse assumption no longer describes who holds what. Watch for it in squeeze setups and obvious manias.

Thin Names and Stale OI

On low-priced stocks with wide strike spacing, a couple of high-OI strikes can dominate the delta read without reflecting the real book, so treat sub-$20 names with suspicion. And stale OI in the roll period right after expiry can register as delta nobody is actually hedging. Expo filters strikes without a live bid/ask; rougher tools do not, which is where phantom lean comes from.

Key Takeaways for Traders

| Step | Action | Why it matters |

|---|---|---|

| Identify | Open Expo at the start of the session. Note the sign of net dealer delta and where it concentrates relative to spot. | The sign is your lean; the concentration tells you where the bid or offer sits. |

| Watch behavior | See whether dips get bought (positive DEX confirming) or rallies get sold (negative DEX confirming). | Price behavior at the lean confirms or kills the read in real time. |

| Align the trade | Trade with the lean: buy dips when the book is a bid, fade rips when it is an offer, stand aside on a flip. | A trade aligned with dealer delta is hedged by the dealer book itself. |

| Pair with levels | Overlay the GEX Call Wall and Put Wall to find where the drift stalls or accelerates. | Direction times levels beats either one alone. |

| Manage risk | Size for the flip. Cut 0DTE size, keep stops tight to the read, re-check after OPEX. | The lean has a short shelf life and reverses fastest near expiry. |

A few honest caveats

- DEX is direction, not timing. It tells you which way the lean points, not the minute the move starts. Pair it with a flow read like Heat or a price trigger.

- Don't trade it without levels. The lean needs a destination. Overlay GEX walls so you know where the drift stalls before you size up.

- It flips fast, especially on 0DTE and near OPEX. A morning bid can become an afternoon offer. Re-read the book whenever the tape changes character.